Market Outlook for Global Shipping – Q2 2025. This article is compiled from a Seatrade Maritime News podcast released in July 2025, hosted by Marcus Hand—a renowned maritime journalist, editor, and speaker with extensive experience in delivering global shipping and maritime industry news.

As the global shipping industry enters the second half of 2025, it continues to navigate a complex web of geopolitical tensions, trade policies, and economic volatility. The sector faces a mix of challenges and opportunities, with developments increasingly shaped by political decisions and regional economic conditions.

Below are the key factors influencing the outlook for container shipping, dry bulk, tanker markets, and shipbuilding.

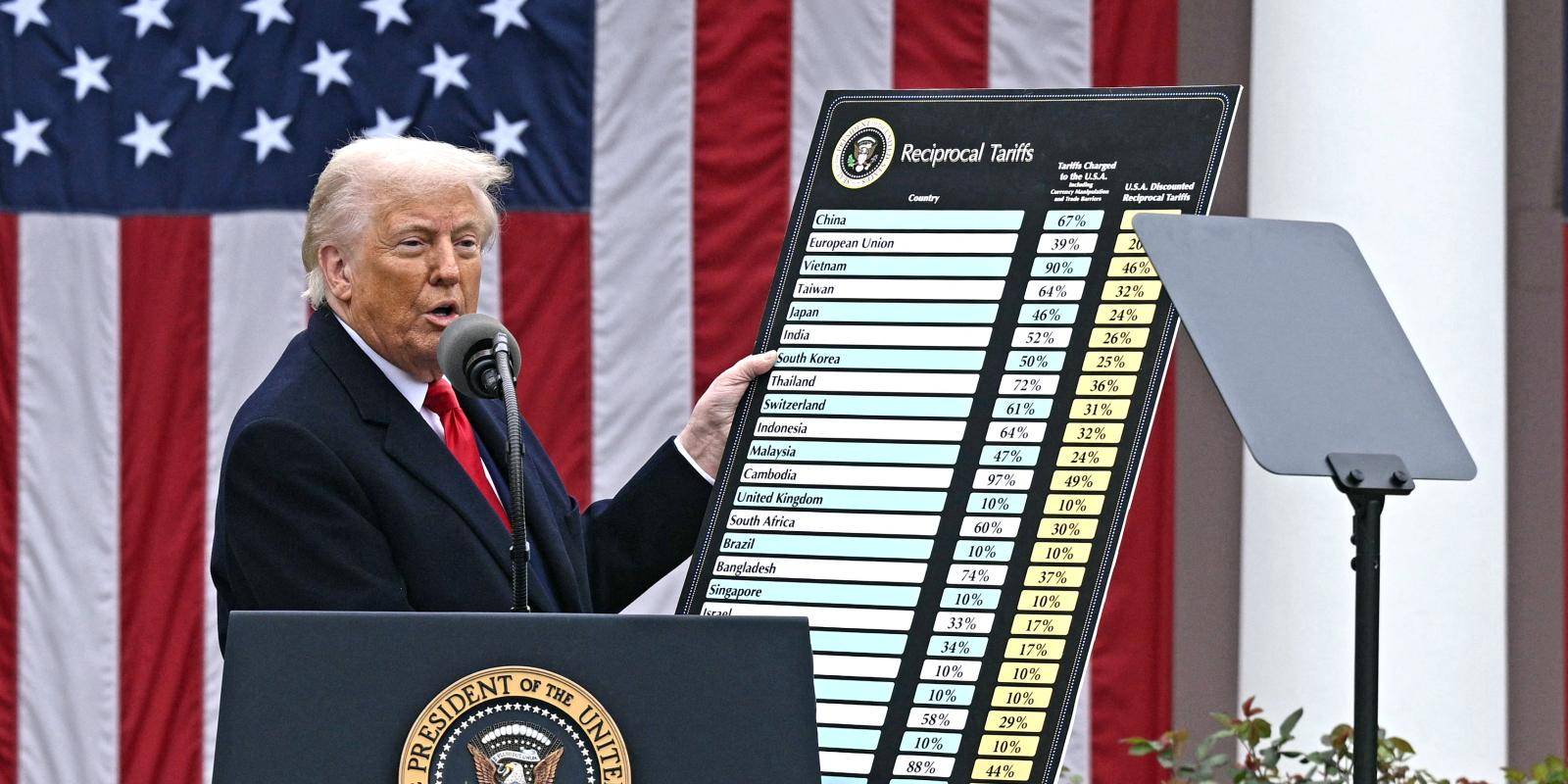

Impact of “On-and-Off” US Tariff Policies on the Container Market. Trade policy remains one of the most disruptive forces in the container shipping market. The fluctuating stance of US administrations—particularly during the presidency of Donald Trump—has historically triggered sharp cycles of volatility in global trade flows.

During this period, while the Biden administration has maintained certain tariff measures, the risk of new or increased tariffs remains. This ongoing uncertainty continues to weigh heavily on the container shipping sector.

In 2025, the potential reintroduction or escalation of tariffs—possibly ranging from 10% to 40%—is viewed as a major risk. Shipping lines are forced to constantly adjust routing strategies, capacity deployment, and inventory planning to mitigate exposure.

As a result, freight rates have shown erratic movements, at times surging due to congestion or front-loaded demand, then easing when negotiations resume or tariff threats temporarily subside.

Planning Challenges Amid Persistent Policy Uncertainty. This unstable policy environment has made long-term planning and investment decisions increasingly difficult for shipping companies and port operators. The lack of predictability raises operational risk and heightens uncertainty across the supply chain, reinforcing the cyclical and fragile nature of the container shipping market in 2025.

Is China Still the Growth Engine of Global Shipping, or Is It Losing Momentum?

For many years, China has been regarded as the primary growth engine of the global shipping industry, particularly in the dry bulk and container segments. However, entering 2025, signs of weakening demand from China have prompted growing questions about whether the country can continue to play the same dominant role.

China’s economy has shown signs of slowing, especially in the real estate sector and industries under tighter regulatory control. Domestic demand for key commodities such as steel, coal, and grain has either declined or stagnated, placing significant pressure on the dry bulk market.

That said, China remains a critical pillar of global trade, particularly through its export-driven manufacturing base and containerized cargo flows. However, growth momentum has clearly moderated, with trade activity becoming increasingly regionally focused within Asia, rather than driven by global markets.

The dry bulk sector, in particular, continues to face challenges due to excess inventories and lower freight rates compared to previous cycles.

In summary, China remains at the center of the global shipping industry. But its role as a growth driver has cooled significantly compared to previous years. This shift is pushing shipping companies and logistics operators to seek new sources of growth in other regions to offset the slowing Chinese demand.

Impact of OPEC+ Production Increases on the Tanker Market

The tanker market, which is closely linked to global oil consumption. Experienced notable volatility in 2025 following OPEC+’s decision to increase oil production.

An increase in crude oil supply from OPEC+ members may lead to lower oil prices. Thereby affecting oil storage and transportation activities. In the short term, overall oil shipment volumes may decline as producers and consumers adjust to lower prices, resulting in reduced demand for VLCC and Suezmax chartering.

However, on the other hand, higher oil output can also stimulate economic activity. Boost energy consumption, and support oil transportation demand in certain regions. This dynamic has helped prevent the tanker market from entering a severe downturn. At present, tanker freight rates have shown a slight downward trend due to oversupply. But geopolitical tensions and strategic energy demand by countries continue to provide a degree of stability to the market.

How South Korean and Japanese Shipbuilders Benefit from USTR Port Fees on Chinese Vessels Calling at US Ports

Amid escalating US–China trade tensions, measures such as tariffs and port fees targeting. Chinese-linked vessels calling at US ports have been implemented. These fees are intended to discourage the use of Chinese-built or Chinese-operated vessels. Creating significant opportunities for South Korean and Japanese shipbuilders.

Shipyards in South Korea and Japan, known for their high-quality construction and advanced technology. Are well positioned to expand their market share in the US. As US ports and operators increasingly prioritize non-Chinese vessels to avoid additional costs. Demand for ships built in these countries is expected to rise. This is particularly evident in segments such as LNG carriers, container vessels, and oil tankers.

In addition, South Korean and Japanese shipbuilders are likely to secure more retrofit, upgrade, and maintenance contracts for existing fleets to comply with evolving regulatory and operational standards. These developments further strengthen their competitive position and broaden their footprint in the US maritime market.

Conclusion

In 2025, the global shipping industry is facing significant challenges driven by geopolitical tensions, trade policies, and regional economic volatility.

US tariff policies continue to create uncertainty for global container trade. While weakening demand from China is weighing heavily on the dry bulk sector. At the same time, OPEC+’s decision to increase oil production is reshaping dynamics in the tanker market. Meanwhile, US measures aimed at restricting Chinese-linked vessels have opened new opportunities for South Korean and Japanese shipbuilders.

Overall, the shipping market in 2025 demands a high degree of flexibility, adaptability, and accurate forecasting. Only by responding proactively to shifting conditions can industry players capitalize on emerging opportunities. While navigating risks in an increasingly volatile environment.

Source: Marcus Hand, Seatrade Maritime News, 2025